Obtaining a tax credit is the next best thing to paying no taxes at all.

The tax code contains over 30 non-refundable tax credits for businesses. These are part of the general business tax credit and are claimed on IRS Form 3800, General Business Tax Credit, and on Schedule 3 of Form 1040. The general business credit is not itself a tax credit, but rather an overall limitation on the total credits that a business can claim each year.

What if you’re a Schedule C business owner who doesn’t have employees and isn’t involved in one of the niche businesses that come with a credit? You’re not necessarily left out of the tax credit bonanza. Here are six tax credits that many Schedule C businesses with no employees can claim (and of course, you can qualify for these credits with employees, too).

- Credit for Increasing Research Activities

The credit for increasing research activities is intended to encourage businesses to invest in scientific research and experimental activities.

Any technological research qualifies, so long as it relates to a product’s new or improved function, performance, reliability, or quality. The research must involve the physical or biological sciences, engineering, or computer science.

You don’t have to have employees to get this credit, because you can claim the credit for 65 percent of the cost of hiring third parties to perform research activities on your behalf, such as outside contractors, engineering firms, or research institutes.

If you qualify, calculating the credit is worthwhile.

- Qualified Plug-In Electric Drive Motor Vehicle Credit

If you purchase a new electric vehicle, you may be able to claim a credit. These include fully electric vehicles (EVs) and plug-in hybrid EVs (PHEVs).

The maximum credit is $7,500, and the minimum is $2,500. But the actual amount depends on the size of the vehicle’s battery. EVs generally get the maximum $7,500, while PHEVs often qualify for less. For example, a Ford Mustang Mach-E qualifies for a $7,500 credit, while a Subaru Crosstrek Hybrid gets only $4,502.

Unfortunately, the credit phases out the year after a manufacturer reaches 200,000 total EV car sales in the U.S.

Tesla and General Motors are the only two manufacturers so far to reach the limit, and the credits for their EVs are now completely phased out. So you won’t get a federal credit if you purchase a Tesla or a Chevy Volt. Toyota and Ford will probably be next to cross the 200,000-EV threshold.

When you claim the credit for a business vehicle, you reduce the vehicle’s depreciable basis by the credit amount. You then depreciate the remaining adjusted basis as you would for any other business vehicle.

- Disabled Access Tax Credit

The Americans with Disabilities Act (ADA) prohibits private employers with 15 or more employees from discriminating against people with disabilities in the full and equal enjoyment of goods, services, and facilities offered by any “place of public accommodation”—this includes businesses open to the public.

The disabled access tax credit is designed to help small businesses defray the costs of complying with the ADA. But you don’t have to have employees to claim the credit. The credit may be claimed by any business with either

- $1 million or less in gross receipts for the preceding tax year, or

- 30 or fewer full-time employees during the preceding tax year.

The amount of the tax credit is equal to 50 percent of your disabled access expenses that exceed $250 in a year but are not more than $10,250. Thus, the maximum credit is $5,000.

- Business Energy Tax Credit

There is a business energy credit based on the cost of qualified energy property used in a trade or business or for the production of income, such as a residential rental building. The credit ranges from 10 percent to 30 percent of the cost of such property.

The credit can be claimed for various types of renewable energy installations, including thermal and geothermal energy, wind turbines, and fuel cells.

But small businesses most often claim the credit for the cost of installing solar panels and related equipment to generate electricity to provide illumination, heating, or cooling (or hot water) in a business structure, or to provide solar process heat.

Unlike the solar credit for homeowners, there is no dollar limit on this business credit. The credit is 26 percent of the cost of solar property whose construction begins in 2020, 2021, or 2022.

The tax code reduces the credit percentage to 22 percent if construction begins during 2023.

- Rehabilitation Tax Credit

The rehabilitation tax credit helps defray part of the cost of rehabilitating historic old buildings. The credit is available only if you rehab a certified historic building or a building located in a registered historic district. The credit can be claimed for commercial, industrial, agricultural, and residential rental historic buildings.

The secretary of the interior must certify to the secretary of the treasury that the project meets their standards and is a “Certified Rehabilitation.” If your building is not already registered as historic but you think it should be, you can nominate it for historic status by contacting your state historic preservation office.

- New Energy-Efficient Home Credit

If you’re a building contractor who builds homes, there is a tax credit just for you. You can get a credit of up to $2,000 for building an energy-efficient home.

The credit is available for all new homes, including manufactured homes, built between January 1, 2018, and December 31, 2021. To meet the energy savings requirements, a home must be certified to provide heating and cooling energy savings of 30 percent to 50 percent compared with a federal standard.

A reduced credit of $1,000 is available for manufactured homes with a heating or cooling consumption at least 30 percent less than a comparable house and with the Energy Star label.

Are More Credits on the Way?

In the news, you have been reading and hearing about the Build Back Better bill that passed the House and is being considered by the Senate. There are lots of tax credits in the bill. But there are three things to know as of December 1, 2021.

- The Senate will likely create and try to pass its own version of this bill.

- If the Senate passes the bill in a different form, the bill will go to a conference with both House and Senate members, who will make more changes.

- Regardless of what happens, we don’t see any changes in the current bill or expect any changes that will affect the information in this newsletter. The changes, if any do become law, will apply to 2022 and later.

Tax Credits for Schedule C Business Owners with Employees

If you hire an employee for your Schedule C business, you can qualify for several valuable tax credits.

Each credit is different, and certain limitations apply to all or most employer tax credits.

Remember, like we said above, tax credits are the best. They beat deductions. Note the difference below (using the 32 percent bracket):

- A $1,000 deduction for wages reduces your income taxes by $320.

- A $1,000 credit reduces your taxes by $680 ($1,000 - $320).

Many tax credits are not available if you hire a person related to you, including children, stepchildren, a spouse, parents, siblings, step-siblings, nephews, nieces, uncles, aunts, cousins, or in-laws.

Eight Valuable Tax Credits for Business Owners

Below are listed the eight non-refundable tax credits that Schedule C business owners can claim when they hire employees.

- Work Opportunity Tax Credit (WOTC)

The WOTC rewards employers for hiring employees from groups the IRS has identified as having “consistently faced significant barriers to employment.”

- Family and Medical Leave Credit

Federal law doesn’t require that you give paid leave to your employees who need to take time off for family reasons (such as the birth of a child) or due to their illness or that of a family member. (A few states require some paid leave that’s funded through payroll deductions.)

But if you choose to provide such paid leave, the federal tax code may reward you with a family and medical leave tax credit.

- Credit for Small Employer Health Insurance Premiums

If you have fewer than 50 full-time-equivalent employees, you are not required to provide your employees with health insurance. But if you elect to do so, you may qualify for the small business health care tax credit. This tax credit is available to eligible employers for two consecutive tax years.

- Credit for Small Employer Pension Plan Start-Up Costs

This credit is for the cost of setting up an employee pension plan, including a new 401(k) plan, 403(b) plan, defined benefit plan (a traditional employee pension plan), profit-sharing plan, SIMPLE IRA or SIMPLE 401(k), or SEP-IRA.

The costs covered by the credit include the expenses to establish and administer the plan and to educate employees about retirement planning.

- Credit for Employer-Provided Childcare Facilities and Services

This little-used credit is intended to encourage employers to provide childcare to their employees. There are two ways to get the credit:

- Build, acquire, rehabilitate, or expand an on-site childcare facility for your employees’ children, and help pay to operate it.

- Contract with a licensed childcare program, including a home-based provider, to provide childcare for your employees.

The second option is more realistic for smaller businesses. Businesses often partner with childcare companies such as the Learning Care Group, Bright Horizons, and KinderCare to offer this benefit.

- Empowerment Zone Employment Credit

Is your business located in one of the designated empowerment zones?

These are areas of high poverty and unemployment identified by the U.S. Department of Housing and Urban Development or the secretary of agriculture.

You might be surprised about which places the government designates as having high poverty and unemployment. It’s worth checking out.

You can claim a credit equal to 20 percent of the first $15,000 in wages you pay to full- or part-time employees who both live and work in an empowerment zone. Thus, the maximum credit is $3,000 per employee (20 percent x $15,000). The employees must work for you for at least 90 days.

- Credit for Employer Differential Wage Payments to Military Personnel

This credit is available if you have an employee in the military reserves who is called to active duty for more than 30 days. If you continue to pay the employee all or part of that employee’s wages while he or she is on active duty, you can claim a credit equal to 20 percent of the payments, up to $20,000.

- Indian Employment Credit

This credit is available only if you hire an enrolled member of an American Indian tribe who both lives and works on an Indian reservation. If this is the case, you may claim a tax credit equal to 20 percent of the wages and health insurance benefits you provide the employee. The Indian employment credit ends December 31, 2021.

When Is a Partner in a Partnership a 1099 Worker?

When the individual production activity of a partner is outside his or her capacity as a member of the partnership, the partnership has two choices:

- Allocate the production income to the partner, and have the partner treat the expenses as unreimbursed partner expenses (UPE).

- Treat the partner as a 1099 independent contractor for the individual production.

Unreimbursed Partner Expenses

As a partner in a partnership, you generally can’t deduct any of the partnership expenses on your individual tax return—the partnership should pay for and deduct its own business expenses.

But if your partnership agreement or business policy forces you as an individual partner to pay for expenses out of pocket, with no reimbursement available, then you can deduct the business expenses in full on your individual tax return as UPE.

Because the UPE is a trade or business expense, it also reduces your self-employment tax.

Treatment as a 1099 Independent Contractor

The tax code is clear on how this works. IRC Section 707(a)(1) states:

If a partner engages in a transaction with a partnership other than in his capacity as a member of such partnership, the transaction shall, except as otherwise provided in this section, be considered as occurring between the partnership and one who is not a partner.

Thus, under this treatment, you would treat that activity as independent contractor activity and report the income to the partner on IRS Form 1099-NEC, Nonemployee Compensation.

The partnership agreement should clearly define how it will treat a partner’s individual production.

Make Extra “Catch-Up” Contributions to Retirement Accounts

After reaching age 50, you can make additional “catch-up” contributions to certain types of tax-advantaged retirement accounts. For the 2021 tax year, this opportunity is available if you’ll be age 50 or older on Friday, December 31, 2021.

Specifically, with an employer-sponsored 401(k), 403(b), 457, or SIMPLE plan, you can make extra salary-reduction catch-up contributions to your account—assuming the plan allows catch-up contributions.

If you are self-employed and have set up a 401(k) plan or SIMPLE IRA for yourself, you can also make extra catch-up contributions to your account.

Finally, you can make extra catch-up contributions to a traditional or Roth IRA.

These catch-up contributions can carry a hefty punch because they are above and beyond the “regular” annual contribution limits that otherwise apply.

The following table shows maximum allowable catch-up contributions for the 2021 tax year:

If you’re married and both you and your spouse are age 50 or older, the amounts shown above can potentially be doubled, assuming both spouses have accounts set up in their respective names.

But with an employer-sponsored plan, maximum salary-reduction catch-up contributions to your account might be less than the indicated amounts—depending on employee participation levels and the terms of the plan.

The Question: How Much Are Catch-Up Contributions Worth?

This is where it gets interesting. While some folks eagerly embrace any chance to contribute more money to tax-advantaged retirement accounts, others might need some encouragement. Those in the latter category may dismiss catch-up contributions as inconsequential unless proven otherwise. Fair enough. So let’s prove otherwise.

Proof: Make 401(k), 403(b), or 457 Plan Catch-Up Contributions

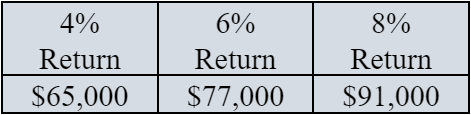

Assume you turn 50 during 2021 and contribute an extra $6,500 to your account for this year, and then you do the same for the subsequent 15 years (for a total of 16 years), up to age 65. Here’s how much extra you could accumulate by that age in your 401(k), 403(b), or 457 account (rounded to the nearest $1,000), assuming the annual rates of return indicated below:

These are substantial amounts. Of course, we are talking before-tax numbers here.

Proof: Make SIMPLE Plan Catch-Up Contributions

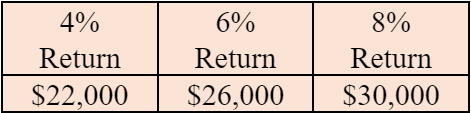

Say you turn 50 during 2021 and contribute an extra $3,000 for this year, and then you do the same for the subsequent 15 years (for a total of 16 years), up to age 65. Here’s how much extra you could accumulate by that age in your SIMPLE plan account (rounded to the nearest $1,000), assuming the annual rates of return indicated below:

Not bad! Once again, remember that these are before-tax numbers.

Proof: Make IRA Catch-Up Contributions

Say you turn 50 during 2021 and contribute an extra $1,000 for this year, and then you do the same for the subsequent 15 years (for a total of 16 years), up to age 65. Here’s how much extra you could accumulate by that age in your IRA (rounded off to the nearest $1,000), assuming the annual rates of return indicated below:

These are before-tax numbers for traditional IRAs but after-tax numbers for Roth IRAs.

If you have questions, don’t hesitate to contact me.

If you own your own business and operate as a proprietorship or partnership (wherein your spouse is not a partner), one of the smartest tax moves you can make is hiring your spouse to work as your employee.

If you own your own business and operate as a proprietorship or partnership (wherein your spouse is not a partner), one of the smartest tax moves you can make is hiring your spouse to work as your employee. College is expensive. Data for the 2019–2020 academic year indicates that the average cost of tuition, fees, room, and board was $30,500. The tax law has provisions to help you cover the costs, including Coverdell accounts, Section 529 savings plans, and Section 529 tuition plans.

College is expensive. Data for the 2019–2020 academic year indicates that the average cost of tuition, fees, room, and board was $30,500. The tax law has provisions to help you cover the costs, including Coverdell accounts, Section 529 savings plans, and Section 529 tuition plans.